In response to the current pandemic, cities across the country are responding as quickly as possible with a myriad of resources to support households and keep businesses afloat. This unprecedented response to an unprecedented crisis is commendable. And, yet, we know it will not be enough. The fallout from the economic aftershock will be severe.

How quickly local economies recover, and families are stabilized, depends not just on response and recovery plans, but ultimately on the resilience of the local economy. Some cities will return to normal faster than others. The speed of recovery will largely be a function of their economy’s resilience and not what happens in the next couple of months.

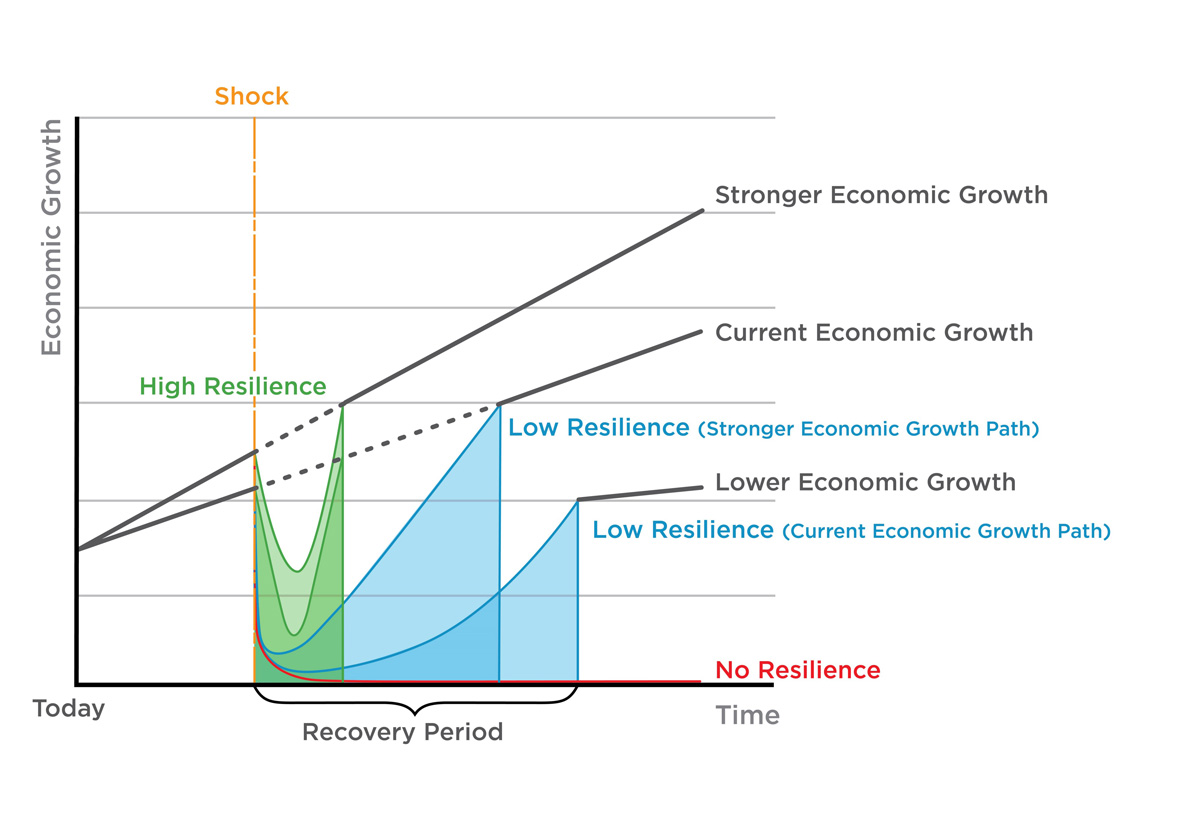

While many definitions for resilience exist, at the core are three basic principles: the ability to adapt to changing conditions, withstand disruptions, and recover quickly.[1]

Resilience and economic growth are both vital for healthy economies in uncertain times. A resilience plan will not grow the economy. It only ensures that cities get back on track — to whatever economic growth trajectory they were on before the crisis — quickly. If a local economy is resilient, the recovery period will be much shorter than an economy with little or no resilience. If a local economy is not resilient, it may never return to its former economic growth path.

History is littered with stories of company towns and cities defined by a single industry that are decimated after major economic shocks. Mill towns in New England, followed by mill towns in the South. The so-called Rust Belt Region. Detroit. Once their primary industries (and largest employers) moved or faltered, the economic foundation of these once thriving areas crumbled.

Getting the Fundamentals Right for Economic Growth

When we advise cities on economic development strategies, we rely on the sound economic growth principles: strong traded-sector industries,[2] skilled workforce, and accessible infrastructure. Cities that want to jump to a higher economic growth plan need to invest in global connections, emerging technologies, and startup ecosystems to bolster innovation. At the same time, they must invest in small local business growth to foster a great place that attracts talent and provides equitable on-ramp opportunities for the entire community.

During this current pandemic, we are witnessing how businesses with a workforce that can work remotely are faring better than those that have had to shut down completely. Our established knowledge-based industries (e.g. software development, engineering) are an important element in rebuilding the economy. However, we caution cities from focusing exclusively on these industries, which typically employ those with degrees and specialized skills not representative of the majority of workers — those that are now unemployed — as a strategy to rebuild the economy.

At the same time, a community should not focus exclusively on local businesses, which cannot thrive without the traded-sector industries that bring new money into the region, provide important contracts for local businesses, and often are major employers that offer higher wages than main street businesses.

Without larger, traded-sector businesses, the local economy shrinks. Without local, small businesses, there is lack of opportunity for residents with lower educational levels and skill sets. Both are vital for a robust economy.

Strong economic growth is based on a system that provides everyone access to wealth creation either through living-wage jobs in established businesses or building opportunity through a new business.

Getting the Fundamentals Right for Economic Resilience

It is important to get the fundamentals right for resilience planning as well. In the race to recovery after the pandemic, we are hearing the term resilience pop up in most conversations, but it is being used by those with little understanding of what resilience really means. The Feeding Cities Group develops pioneering resilience plans based on the fundamentals of risk management and sustainability. Key resilience components for cities include:

· A business base that includes diverse industrial sectors, representing similar shares of economic output and employment.

· A diverse range of businesses in terms of size and ownership, from main street businesses to corporates.

· Small businesses in all life cycle stages, from start-ups to mature enterprises.

· An effective entrepreneurial ecosystem that will foster new entrepreneurs, get the owners of closed businesses into start-up mode, and help small businesses pivot and grow through uncertain times. The support will intentionally include underrepresented entrepreneurs (woman, people of color and veterans).

· Small businesses need more than infusions of capital to be resilient. They need technical assistance, business management education, and access to new customers and suppliers.

· Healthy anchor organizations such as a university, college or hospital that actively support local hiring and purchasing from local businesses.

· Effective workforce organizations that can rapidly connect the unemployed to new jobs (in new industries) and provide efficient job training as needed.

· A labor force with new skills to navigate unprecedented job insecurity.

These fundamentals will ensure that businesses stay open, failed business owners start new enterprises, some move from unemployment to entrepreneurship and others to new jobs. Resilient cities will also invest equally in addressing chronic stressors associated with economic inequality, which plagues all of our cities: poverty, unemployment, health disparities, racial biases, etc. As the current pandemic is showing once again, disasters disproportionately impact our most vulnerable populations.

Cities will need to address those left behind before they can jump forward.

A Call to Action

We challenge cities to re-evaluate both their economic development strategy and resilience plan in light of this new economic landscape that is at risk of leaving a significant portion of our population even more disenfranchised. Within the new CARES Act, the federal Economic Development Administration (EDA) has allocated $1.5 billion for grants through its established Economic Adjustment Assistance (EAA) program, which includes 80–100% funding for Comprehensive Economic Development Strategies (CEDS).

We are currently working with visionary leaders in Portland, Oregon, on a CEDS that fully integrates a resilience perspective, and is poised to set an example of how a region can foster a strong economy that serves everyone.[3] This pandemic will challenge all of us, but it also serves as an opportunity for city leaders to take a new approach — one that integrates resilience into economic development strategies and makes regions more prepared for inevitable future shocks.

[1] “Resilience,” U.S. Department of Homeland Security, accessed April 3, 2015. http://www.dhs.gov/topic/resilience.

[2] Traded-sector industries, sometimes called export industries, create products or ideas that sold outside a region and bring new money into the regional economy while offering family-wage jobs. They often invest in research, encourage creation of new startups, and support smaller companies within product supply chains.

[3] The Portland Metro CEDS is led by Greater Portland, Inc., which serves as the region’s Economic Development District (EDD), and Metro the regional Metropolitan Planning Organization (MPO).

Alisa Pyszka is the President of Bridge Economic Development, a consulting firm that works with cities, counties and regional organizations to deliver economic development strategies and action plans.

Kim Zeuli, PhD, is the Founder and Managing Director of The Feeding Cities Group, a social enterprise dedicated to advancing equitable urban resilience using pioneering frameworks based on economic theory and practice.